Airbnb co-founder and CEO Brian Chesky took to X (formerly Twitter) to argue that real-world asset tokenization should be judged by how much ownership friction it removes and whether holders can trust whoever holds the underlying asset.

[Editor’s note: He announced no Airbnb tokenization product.]

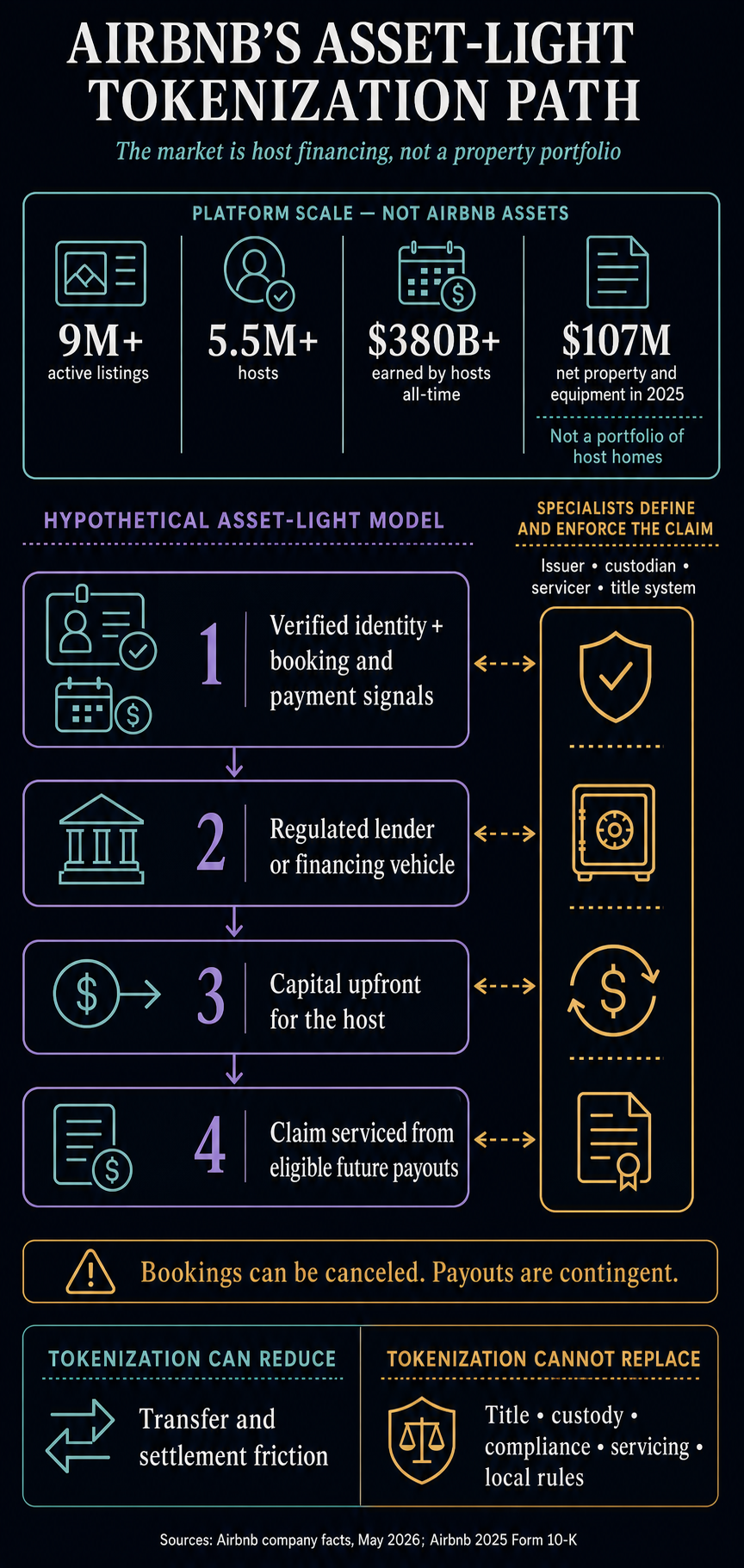

Applied to Airbnb, his thesis points to a counterintuitive opportunity. The company could use its marketplace reach and identity, along with booking and payment signals, to support regulated financing for hosts, while separate lenders, issuers, special-purpose vehicles, custodians, and title systems define the legal claims and keep the homes off Airbnb’s balance sheet.

Chesky cited fractional access, faster settlement and markets that stay open as potential gains. He then connected the trust problem to Airbnb’s experience persuading strangers to share homes, later adding that “Trust is everything”.

His thoughts came after he shared a video of Robinhood CEO Vlad Tenev, who argued that productive assets such as tokenized stocks, futures, and private companies would drive crypto’s growth as financial markets move on-chain.

Airbnb’s scale can make the approach look deceptively like a property portfolio. Its May 2026 company facts report more than 9 million active listings, more than 5.5 million hosts and more than $380 billion earned by hosts since the platform began.

Airbnb’s 2025 annual filing says the company records rental revenue as an agent because it does not control the right to use host properties, fulfill hosts’ rental promises, bear inventory risk or set host prices. Its stay revenue primarily reflects service fees.

Airbnb reported $107 million in net property and equipment as of Dec. 31, 2025, but that balance does not represent vacation homes listed on the platform. Its gross property and equipment consisted mainly of software and leasehold improvements, while a remaining $49 million category combined buildings and land with computer equipment, construction in progress, and office furniture.

Airbnb’s terms also state that Airbnb and its affiliates do not own, control, offer, or manage the listings on the platform

What it has is distribution, trusted identities, and operating data around host activity.

Host payout financing offers the clearest asset-light path

Airbnb has already shown how platform data can support financing without turning the company into a lender or landlord. In 2018, it allowed participating hosts to provide Airbnb-generated proof of income to specialist mortgage lenders.

A future structure could build on that logic, although Airbnb has announced no such plan.

Hypothetically, a host could receive capital upfront in exchange for tokenized claims on eligible future Airbnb payouts, with the tokens defining payment rights and distribution terms.

Alternatively, a financing vehicle could raise capital from investors and fund hosts, and issue tokens representing investor claims against the vehicle rather than against Airbnb or the underlying property.

Airbnb might, with the necessary agreements and host consent, provide verification signals, distribute the product, or route eligible payments. The lender or investor would have the rights granted by the on-chain financing contracts against the host or vehicle, not an automatic claim on Airbnb or the home.

However, before a stay becomes eligible, a booking may be canceled or changed, and the expected payout may shrink or disappear. Any financing contract would need rules for eligibility, refunds, chargebacks, occupancy changes, payment control, servicing, privacy, loss allocation, and shortfalls.

Different legal structures would produce different obligations. The Consumer Financial Protection Bureau treats some sales-based financing tied to anticipated revenue as business credit. Other structures could trigger securities or additional laws depending on their terms. A blockchain record would not necessarily settle that classification.

Airbnb’s options diverge sharply once the legal claim and balance-sheet exposure are made explicit:

StructureInvestor or lender claimPossible Airbnb roleFit with current modelMain frictionContingent host-payout financingA contractual claim against a host or financing vehicle, potentially serviced from eligible future payoutsHypothetical data, verification, distribution or payment-routing supportStrongest analytical fitCancellations, eligibility, privacy, servicing and loss allocationSPV-based property equityAn interest in a vehicle that owns or evidences the property interestHost data and distribution supportModerateTitle, liens, custody, securities compliance, governance, maintenance, vacancy and local rulesPlatform fee or minority participationRights defined by the issuer or property vehicle, not by Airbnb’s listing networkAirbnb could earn a fee or separately hold a minority stakeFee-only is lighter; a stake adds balance-sheet exposureValuation, conflicts, capital exposure and governanceAirbnb buys homes and sells interestsThe security or SPV interest granted by documents tied to company-controlled propertyOwner, operator and issuer or sponsorLeast consistent with the current modelCapital, vacancy, maintenance, governance and housing-policy riskReservation, membership or loyalty tokenOnly the access or benefits defined by its operative termsProduct and distribution platformPotentially compatible, but not an ownership marketThe label alone determines neither ownership, yield nor legal status

To be clear, none of these structures is an announced Airbnb product. The first structure best preserves the company’s role as a marketplace. Property equity could still be asset-light for Airbnb if a separate vehicle held title, but it would leave much more off-chain work. A loyalty product might be useful without creating an investable claim at all.

A token cannot supply the missing legal rights

Current tokenized stocks already show why the legal wrapper does the heavy lifting. Tenev’s Robinhood already has its live Chain designed for tokenized real-world assets. Its new Stock Tokens, however, are debt securities issued by Robinhood Assets in Jersey. Holders have contractual rights under that debt instrument, but no legal or beneficial ownership or shareholder rights in the referenced company.

A January SEC staff statement describes issuer-sponsored tokenized securities and third-party models, including custodial and synthetic structures. The nonbinding statement applies to instruments that are securities, not every tokenized asset. For an instrument that is a security, moving it on-chain does not remove federal securities-law requirements; its structure still determines what the holder owns or is owed.

For property equity, the token cannot create clean title, clear a lien or define investor governance by itself. The off-chain entity would still need to hold or evidence the property interest and allocate maintenance, vacancy and local accommodation obligations.

Those burdens make Airbnb buying properties and selling interests the most significant break from its agent model. It would add the inventory, capital, and operating risks that the platform currently largely leaves with hosts, along with new conflicts between investors and the supply side of the marketplace.

With contingent payouts, the real challenge sits in the contract. Airbnb could stay out of the ownership chain while clear eligibility rules, consent, payment controls, and an enforceable claim keep hosts, investors, and service providers aligned. Its trust and operating data could support that structure while specialist firms hold and enforce the claim.

Crypto exchanges are already becoming distribution channels for exposure to traditional assets. Airbnb’s possible advantage would be different: verified history behind host activity and a payment relationship with the people seeking capital.

The concrete signal to watch is a regulated partnership that uses verified booking history to finance contingent host payouts while specialists own, service, and enforce the claim.

An “Airbnb coin” or tokenized listings would take the company somewhere else entirely. A financing partnership offers a simpler way to test whether Chesky’s ownership idea works without disrupting Airbnb’s marketplace model.